A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

Historically, determining the correct amount to invest in a 529 college savings account to cover the exceedingly growing cost of higher education (without overfunding it) has been a challenge.

The 529 Plan has three primary benefits:

- Tax-deductible contributions on your state (not Federal) tax return.

Note: these rules vary by state and not all states allow for a tax deduction. - Tax-deferred growth.

- Tax-free withdrawals for qualified education expenses.

These tax benefits are great, but what happens to the 529 funds when a beneficiary decides not to pursue higher education? Or perhaps they receive more scholarship money than anticipated? Or grandparents have been funding additional accounts, and the account is left with a sum of money that is unable to be used for educational purposes? There are several options in these circumstances. Overfunded 529 assets can be transferred to another beneficiary to use for education purposes without tax consequences, or the account owner (usually the parent) can choose to withdraw excess funds and pay income tax (at their tax rate) and an additional 10% penalty to use the cash for their own purposes. However, these options, which result in taxes and penalties, are not ideal for the beneficiary, who is likely trying to kick start a career and start saving for retirement.

The Secure 2.0 Act, a comprehensive retirement reform federal law enacted in the final days of 2022, introduced several new provisions aimed at enhancing retirement savings and financial security. Among these, one of the most notable is a provision that allows for the tax-free transfer of funds from 529 college savings plans to Roth IRAs for the beneficiary. This new rule provides greater flexibility and potential tax advantages for account holders, making it a significant development for those looking to help children (or grandchildren) with both education and retirement. This blog will explore the rules and qualifications for this transfer, as well as the state tax implications.

Rules and Qualifications for Rolling over 529 Plans to Roth IRAs

The provision in the new law that allows the transfer of 529 plan funds to Roth IRAs has several conditions to ensure proper compliance and to prevent abuse of the tax advantages associated with both 529 plans and Roth IRAs.

Here are the key points to consider:

- Beneficiary Restrictions: The transfer can only be made to the beneficiary of the 529 plan. This means that if a parent is the custodian on a 529 plan and their child is listed as the beneficiary, the funds must be transferred to the child's Roth IRA, not the parent's.

- The “15-Year” Rule: The 529 plan must have been open for at least 15 years before any transfers can be made. This rule is designed to prevent the use of 529 plans primarily for Roth IRA funding rather than for their intended purpose of education savings.

- Lifetime Maximum: At this time, the lifetime limit on these 529 rollovers is $35,000. Further, there is an annual funding limit. In a given year, the most that can be transferred from a 529 plan to a Roth IRA is currently $7,000 ($8,000 if age 50 and above). This cap ensures that the provision is used to support retirement savings rather than as a primary retirement savings vehicle.

- The “5-Year” 529 Contribution Rule: Contributions (and their earnings) made to the 529 plan within the last five years are not eligible for transfer. This stipulation further ensures that the 529 plan has been used primarily for its intended purpose before being redirected to a Roth IRA.

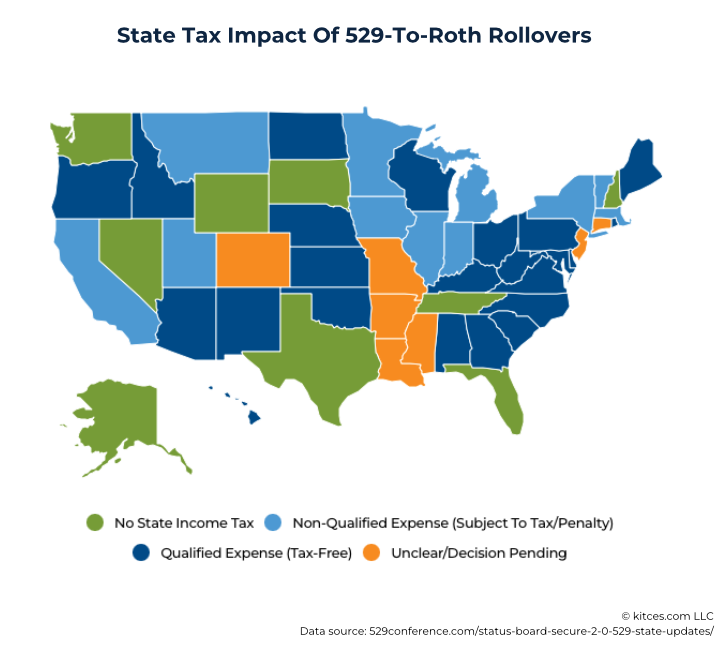

State Tax Implications

If qualifications are met, rolling 529 plan assets to a Roth IRA can be tax-free on a federal level. State tax implications, however, can vary and should be carefully considered. As illustrated below, 32 states (9 of which are income tax-free states) will treat 529 rollovers to Roth IRAs as a qualified tax-free distribution, while 11 states treat these rollovers as non-qualified expenses subject to income tax and penalties. The 7 remaining states (plus Washington D.C.) have yet to decide how they want to treat the rollovers.

State-Specific Rules: Each state has its own set of rules governing 529 plans and IRAs. Consult with your Burney Wealth Management Advisor to determine the rules for your state and how to proceed.

Income Limits on Roth Contributions vs 529 – Roth Transfer Rules

Traditional Roth IRA contributions are limited based on the taxpayers’ Modified Adjusted Gross Income (MAGI). Single Filers with a MAGI of more than $165,000/ Married Filing Joint Filers with a MAGI of more than $246,000 cannot contribute to a traditional Roth IRA. When transferring from a 529 to a Roth IRA, however, there is no income limitation. This is a significant potential benefit for higher-income 529 holders.

i.e. Johnny is 35 years old and earns $500,000 as a software salesman. He cannot contribute to a Roth IRA in the traditional sense, but he could transfer $7,000 from his existing 529 into his Roth IRA if the other criteria listed above are satisfied.

Additional Planning Considerations

- Strategic Use of 529 Plans: The ability to transfer funds tax-free to a Roth IRA provides an additional layer of flexibility for 529 plans. It allows families to save for education with the confidence that at least a portion of unused funds can be redirected toward retirement savings without penalties.

- Retirement Savings Boost: For younger beneficiaries, transferring 529 plan funds to a Roth IRA can provide a significant head start on retirement savings. Given the potential for decades of tax-free growth, even modest transfers can compound significantly over time.

- Financial Planning Integration: Integrating education and retirement planning can lead to more comprehensive financial strategies. This provision encourages families to think holistically about their long-term financial goals and how to best utilize available tax-advantaged accounts.

Conclusion

As illustrated above, the recent change to federal law allowing the transfer of 529 college savings plan funds to Roth IRAs introduces a new, creative way of viewing education planning and retirement planning all at once. While this provision is not as flexible and limitless as back-door Roth contributions or Roth conversions, it is designed to offer a solution to the fear of overfunding 529 accounts. By understanding the rules and qualifications, considering state tax implications, and being mindful of the five-year rule for Roth IRA contributions, families, working with their financial advisor, can make informed decisions that enhance both education and retirement savings. This feature exemplifies the evolving nature of financial planning, offering greater flexibility and opportunities for those looking to maximize their savings potential across different stages of life. Consult with your Burney Wealth Management Advisor to evaluate the benefits of a 529 Plan to Roth IRA rollover in your financial plan.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.