A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

Shortly after graduating college last May, I began my first full-time position working as a Client Service Associate at Burney Company. Although I felt prepared to begin my professional career, there was also some anxiety that came along with this new and unfamiliar chapter. With 16 years of education behind me, my routine would now be shifting. While I used to rely on my course syllabus as a guide to success, I found myself missing a laid-out path to tackle the various financial changes that come with a new job. College provided me with so many valuable skills, but my curriculum did leave out a few important details. I’ll be breaking down some of the daunting topics that come along with being a financially responsible adult.

Step 1: Make a budget

One of the most intimidating questions I faced was a simple one: where do I begin? If you have just started your first full-time job, you’ll have a lot of new items thrown your way, including a paycheck. Deciding how to put your money to use in the best possible way can seem like an overwhelming task. Making a budget will help you get organized and utilize that paycheck to its full potential.

Take this with a grain of salt. I don’t mean to count out every penny and skip out on fun times with your friends. Balance is always important; however, it can be helpful to have an idea of where your money is going. Burney Wealth Management offers an interactive online portal that allows users to view all their finances in one place. Tracking your spending will give you a good sense of what your financial picture looks like and where you can cut down costs. The first time you see your spending habits may be alarming, but let it be a wake-up call. I personally had to cut down on my Starbucks trips after realizing that all those $5 coffees add up.

Step 2: Make saving a priority

Your future self will thank you immensely if you make a conscious effort to save from the get-go. Saving is a broad category, so let’s break it down a little more:

Emergency Fund: This should be your first saving goal. It is recommended to leave yourself three months of living expenses in an untouched account. This extra cushion will be critical if you are ever facing unexpected expenses.

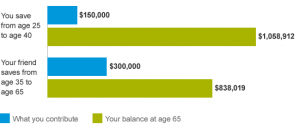

Retirement Funds: As a new member of the workforce, retirement may not be at the forefront of your mind. While you have a long way to go, you should get a jump start on retirement savings. In fact, time is your greatest asset. With the power of compounding interest, starting early will give you more flexibility later on.

Source: Vanguard

Generally, saving 15% of your income into a retirement account is a good starting point, with the goal to increase that by 1% every year. There are several different plans to accomplish this:

- 401k (or any employer-sponsored plan): Your new job might include a retirement plan as part of its benefits package. You should be able to contribute to this plan directly every month, making it an easy way to save. If your employer matches your 401k contributions, try to maximize this feature to its full potential, or you’ll be missing out on free money.

- Individual Retirement Account (IRA) or Roth IRA: Depending on your income level, an IRA or Roth IRA may also be a great route for retirement savings. This is an account you can open on your own at a financial institution, such as TD Ameritrade, to save for retirement. An IRA differs from other accounts because it offers users great tax benefits. When referring specifically to a Roth IRA, contributions are made with after-tax money. This means you’ll take care of your taxes upfront, let your money grow tax-free, and withdraw it tax-free at the time of retirement. If you’re in a low tax-bracket right now, it may be a good option to consider.

Step 3: Invest

Another key to financial success is investing into a taxable account. Building the habit of investing in the market regularly, even if it’s as little as $25 a month to start, can make a significant impact on your future wealth. There are affordable ways to get diversified in the market, specifically through low-cost index funds. This is a great first step for a new investor looking to get started. Make a consistent effort to put some money into this account every month.

Step 4: Stay involved with your finances

This is a very brief and basic start to your financial future. The reality is that your finances will continue to grow in both value and complexity. In the near future, you may plan to buy a house or start a family. Stay proactive and aware of your situation so you can make appropriate adjustments. Even with just these beginning steps, you will help yourself greatly in your journey to financial success.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.