A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

Long-term care can be overwhelming to plan for, but the reality is an individual who turns 65 today has a 70% chance of needing a type of long-term care during their lifetime. Not planning can cause more stress on family members or drain saved retirement funds. With all the information out there, it’s important to review the different paths you can take and their potential costs as your long-term care needs evolve.

Adult Day Care

Adult day care is a type of assisted living care that has minimal involvement. It allows an individual to live in their own residence and commute to the center during the day. The point is to alleviate pressure on other caregivers and provide support for people who need extra assistance during the day but not around the clock care.

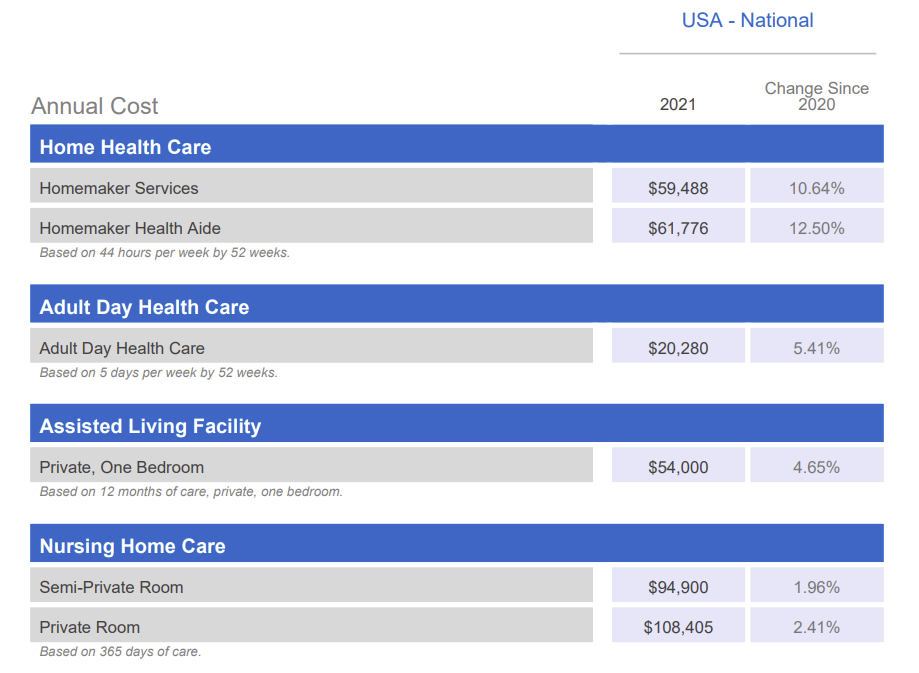

Assisted Living Facilities

Assisted living facilities are a more involved option compared to adult day care. These centers require an individual to move into the center to help with any needed activities of daily living (ADLs). These include bathing, showering, dressing, transferring, walking, using the restroom, or eating. This care aims to keep an individual’s level of independence while also providing the full-time personalized support they need. It also creates a community environment for the residents to participate in.

Skilled Nursing Homes

Skilled nursing is the most involved type of care that is listed. This is only needed for full-time care by a registered nurse that can’t be delivered to an individual’s home. Typically, this care is needed later in a long-term care path but can vary based on specific situations. For example, are there caregivers at home available to help or are there any conditions that you know you are predisposed to? These facilities are also the most expensive type of care which are generally offered with semi-private and private rooms as options.

Home Health Care

Home health care is the most versatile of the options. The coverage can be for a few hours a week up to 24 hour support offered within an individual’s home. There are also levels within home health care. Homemaker services focus on assisting with housekeeping tasks and assisting with ADLs, this is comparable to assisted living care. Home health aide services focus on assisting with medical equipment and providing a more intense level of care, comparable to skilled nursing homes. Both services are flexible, alleviate pressure on spouses or other in-home caregivers, and give the individual personalized care within their residence.

Costs

All prices are based on the national average cost of long-term care from the Genworth Cost of Care Survey in 2021. The cost of care varies by state and region so look at this survey to see what your specific care costs would be for your area. This can also be a factor if you are willing to move to another area that may have more beneficial long-term care pricing.

What Is Right For Me?

There is not a single right answer for long-term care what type of care will be best for you, although there are a few questions you can use to preemptively consider your future needs:

- What is your family’s health history?

- Are you planning as an individual or as a couple?

- Are you willing to relocate?

- What do you want your end of life to look like?

- Do you have any family who can help provide or manage care?

- What assets and savings accounts do you currently have?

After considering these questions, think about the potential long-term care needs that you might have. Assess with a financial planner what kind of funding could be right for you and your long-term care plan. Overall, keep in mind that there are many different long-term care options to choose from and your long-term care needs will develop and change as you progress in life.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.