A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

Almost 6 years ago, I attended one of my first lectures at the University of Mary Washington. Eager and a little nervous, I arrived early for Accounting 101. I do not remember a whole lot about that first lecture, but I do remember the professor insisting everyone attend the last class of the semester. We were told, “I don’t care if you are sick or break a leg, just make sure you attend that class.”

Why was it so imperative to go to the last class before our final exam? He was going to teach us about the importance of compound interest and the benefits of investing in the markets.

What is compound interest?

Compound interest is best explained with an example: If you start with $100 and it grows 10% in a year, your account earned $10 and is now worth $110. If your account grows at the exact same rate the following year, you earn $11, one dollar more than it did the year prior even though the rate of return was the same. The longer this trend is able to continue, the more your money will grow.

Over long periods of time, the extra amount earned from a growing investment makes a huge difference, resulting in exponential growth and wealth creation. It is a tool that helps battle wealth eroding factors such as rising cost of living and inflation.

Why is understanding compound interest important for a young professional?

As my colleague Brenna Surette explained in her post, What They Don’t Teach You in College, retirement may not be the most pressing priority in a young person’s life. While the future does seem far away, it is important to recognize the cost of delaying investing. The chart below from CNBC illustrates the consequences of starting later.

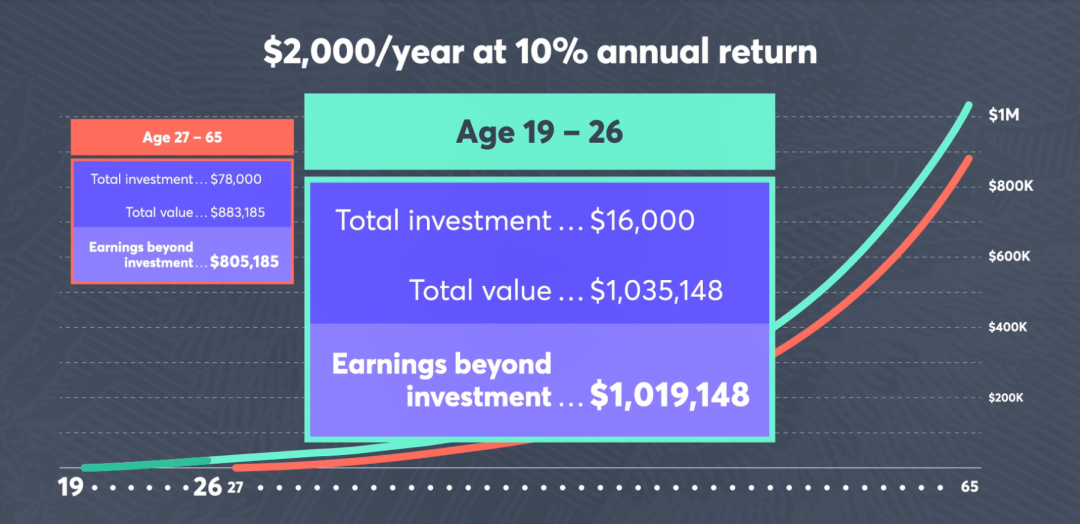

Assuming a retirement age of 65, a 10% annual rate of return, and two investors who start saving at different times in their lives:

Individual 1 is a 19-year-old who puts $2,000 away every year till the age of 27, and then lets that money grow until age 65

Individual 2 is a 27-year-old who puts away $2,000 away every year until the age of 65

Individual 1 put away money for just eight years while individual two put away money for 38 years…but individual one still ended up with $213,963 more wealth because they started earlier and were able to reap the benefits of compound interest for a longer period of time. Individual 2 would have to invest significantly more money just to catch up, and the gap grows wider the longer they wait. Young working professionals are clearly incentivized to begin saving and investing as soon as possible, even with smaller dollar amounts.

My accounting professor wanted as many students as possible in his final class because taking advantage of compound interest can allow individuals to retire how they want, buy the house they want, and achieve whatever other financial goals they set. For a young person, time is their most valuable asset class. It is never too early for the next generation to start investing.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.