A team to guide you

Our team of advisors guide you through various retirement scenarios, quantify your goals and plan for life’s uncertainties before crafting a retirement plan that aligns with the future you envision.

So far in our Medicare 101 series we have covered the Medicare program basics and reviewed the details of Medicare Part A. Next up is a closer look at the second layer of the Medicare system, Part B.

While Part A provides coverage for hospital, in-home, and institutional services, Part B primarily deals with doctor’s services and preventative care.

Part B– What does it cover?

Medicare Part B is designed to provide the following services:

- Preventative Care: Part B coverage incentivizes you to stay healthy by covering the following preventative services:

- Annual wellness exams

- Many types of preventative screening exams such as mammograms and colonoscopies

- Flu shots

- Smoking and obesity counseling

- Medical Services: In the event that health care is needed, Part B will step in and provide for the following:

- Medically necessary doctor’s visits (even while staying in the hospital, covered under Part A)

- Approved procedures such as x-rays, casts, stiches, or outpatient surgeries

- Home health services

- Durable medical equipment

- Ambulance services when other transportation options would risk your health

Part B – What does it cost?

Unlike Part A, which is free to most seniors, Part B does come with a monthly premium cost.

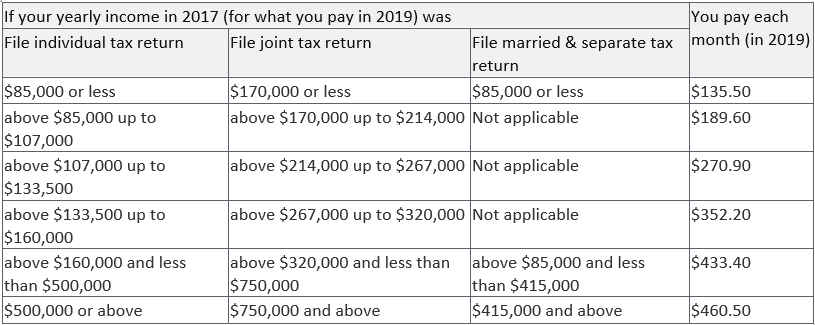

The base monthly premium for 2019 is $135.50/month per person. If you are collecting Social Security this amount will be automatically deducted from your monthly benefit. If you are delaying Social Security benefits then you’ll receive a bill in the mail with various payment methods available.

There is also a potential additional monthly premium surcharge, knowns as the income-related monthly adjustment amount (IRMAA), that is applied on top of the $135.50. This adjustment is based on the modified adjusted gross income reported on your IRS tax return from 2 years ago:

Source: https://www.medicare.gov/your-medicare-costs/part-b-costs

On top of the monthly premiums (and relevant adjustments listed above) there is also an annual deductible of $185 in 2019.

Once your deductible is met, you will also pay 20% of the Medicare-approved amount for doctor services, outpatient therapy, and durable medical equipment.

Note: You will want to have ample retirement resources available for coinsurance and deductibles under Medicare Part A and B in retirement. This is a very important part of the retirement planning process and a key deliverable of a knowledgeable advisor.

What is NOT Covered Under Medicare Part A and B?

Medicare doesn’t cover everything. If you need certain services that aren’t covered under Medicare Part A or Part B, you’ll have to pay for them yourself unless:

- You have other coverage (including Medicaid) to cover the costs

- You’re in a Medicare Advantage Plan that covers these services (we will discuss Medicare Advantage plans in our next post)

Some of the items and services that Medicare Part A and B do not cover include:

- Most dental care

- Eye exams related to prescribing glasses

- Dentures

- Cosmetic surgery

- Massage therapy

- Routine physical exams.

- Acupuncture

- Hearing aids and exams for fitting them

- Long-term care.

This wraps up our summary of Medicare Part B. Remember, an important consideration of a comprehensive retirement plan is accounting for the various parts of Medicare and what they mean for your out-of-pocket costs.

To learn more about Medicare and the specifics, the government has a great resource that it publishes annually, titled Medicare & You that reviews the Medicare system and coverages in greater detail.

The Burney Company is an SEC-registered investment adviser. Burney Wealth Management is a division of the Burney Company. Registration with the SEC or any state securities authority does not imply that Burney Company or any of its principals or employees possesses a particular level of skill or training in the investment advisory business or any other business. Burney Company does not provide legal, tax, or accounting advice, but offers it through third parties. Before making any financial decisions, clients should consult their legal and/or tax advisors.